- Home

- Shareholder Engagement of Corporate Japan [Second Edition]

Part 4 Corporate Governance and Sustainability

Chapter 1 Corporate Governance Reform and Japanese Companies

Yuzo Fujishima

When I first became involved in the field of corporate governance around the year 2000, this area was viewed with suspicion in Japan's capital markets, akin to a “black ship” from a foreign land. Over time, however, it came to be regarded as a set of sacred principles – almost like “golden rules.” During this process, numerous authorities have emerged, and various theories on corporate governance reflecting the times have been discussed. In this chapter, we will refrain from discussing its chronological trend and instead, return to the fundamentals of what corporate governance is and how we should approach it, delving into its “substance” and even its “essence.”

1. Correctly understanding corporate governance

Corporate governance is often translated into Japanese as “corporate management,” but this does not imply that top management governs the company. In particular, listed companies are supported by raising capital through the capital market, and in economic terms, shareholders, who are pure investors, are equivalent to the owners of the company. From the shareholders’ perspective as owners, the purpose of corporate governance is to verify whether a company’s management strategies are appropriate and whether it is being managed to achieve performance growth and, ultimately, improve stock prices. It is essential to correctly understand the discussion regarding the “form” and “substance” of corporate governance from this “shareholder = owner” perspective.

Needless to say, “form” refers to institutional design measures, such as ensuring board independence (including the number and proportion of outside directors) and establishing a compensation committee, whether mandatory or voluntary. The issue is “substance.” While there is a general framework that the “value” created by a company is its substance, it is sometimes argued that this “value” should contribute to society as a whole and benefit various stakeholders. However, since the owners of a company are its shareholders, there is no room for doubt that the primary purpose of a company is to create “shareholder value.” Companies fulfill the “substance” of corporate governance by conducting business that benefits various stakeholders and contributes to society as a whole while also providing economic value to shareholders. To achieve this, it is necessary to establish the “form” of governance, such as independence, as a means to that end.

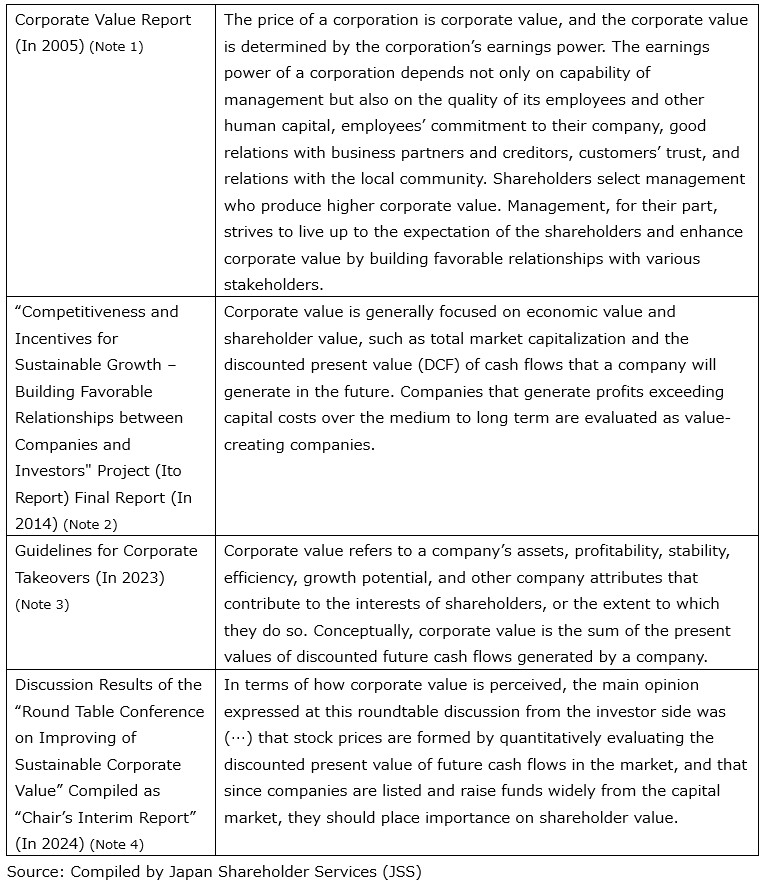

Figure 4-1-1: Definition of corporate value in various initiatives by Ministry of Economy, Trade and Industry (METI)

The “substance” of shareholder value is nothing other than the expansion of business performance and the improvement of stock prices. In today's capital markets where institutional investors play a central role, sustainable stock price increases are unlikely without the expectation of long-term performance growth. The expected level of future cash flows is reflected in the shareholder value at present. Performance growth that leads to stock price increases is achieved through the maintenance of excellent capital productivity and the development of attractive investment opportunities and is evaluated in the capital markets through P/B (= ROE×P/E).

Furthermore, when viewed from an ESG perspective, E (environmental) and S (social) can be regarded as long-term management issues that reflect future growth potential and risks. These elements are directly linked to future cash flows. On the other hand, G (governance) plays a leading role in enhancing shareholder value by driving E and S and can be described as a “foundation” that goes beyond mere “form” to bring out “substance.”

2. Japan's capital market, which lacked governance

In the postwar period, it would not be an exaggeration to say that there was certain period that Japan's capital market was actively working to undermine corporate governance. The board of directors which had become a mere formality with its management-centric structure, auditors whose authority was reduced to plain compliance audit, and shareholder meetings rendered powerless by cross-shareholdings – all these elements stripped away the supervisory functions that were supposed to address management incompetence and inaction, leaving them completely hollowed out. Despite steady stock price increases, achieving expansion of performance in an economic environment of robust external and domestic demand was easily accomplished through management by imitation and adherence to precedents. Japanese companies became complacent with praise such as “Japan as Number One,” and when asked about the secret to their success, they resorted to illogical and unscientific phrases like “strengths not reflected in numbers” or “the unique spirit of the Japanese people.”

However, after the high-growth era ended and the bubble economy collapsed, management faced a drastically transformed environment, driven by intensifying global competition and low domestic growth. Without painful measures, capital productivity cannot be improved, and without taking risks, growth opportunities cannot be obtained. The stock price ruthlessly reflects management's incompetence or inaction, and the global disparity in corporate strength measured by market capitalization further exacerbates the challenges faced by management. In such circumstances, if corporate governance had functioned effectively, it might have been possible to establish a management structure led by optimal executives and reward them with appropriate incentive-based compensation, thereby striving to enhance shareholder value. However, the neglect of shareholder-focused corporate governance contributed to the decline in the global presence of Japanese companies.

Meanwhile, in the United States, corporate governance reforms centered on institutional investors and focused on shareholder value have progressed, creating an overwhelming gap in global competitiveness and market capitalization between Japanese companies and their US counterparts. At times, excessive focus on short-term stock price increases or shareholder returns has led to scandals and credit crises that shook the entire capital markets. However, reforms such as the Sarbanes-Oxley Act following the Enron scandal, and the Dodd-Frank Act following the global financial crisis, the capital markets have demonstrated a high degree of corrective capacity.

Companies have sustained long-term growth in shareholder value by continuously refining corporate governance to adapt to changing circumstances. Probably it would not be an overstatement to say that the difference in competitiveness stems from the difference in corporate governance.

3. Market discipline brought about by Abenomics

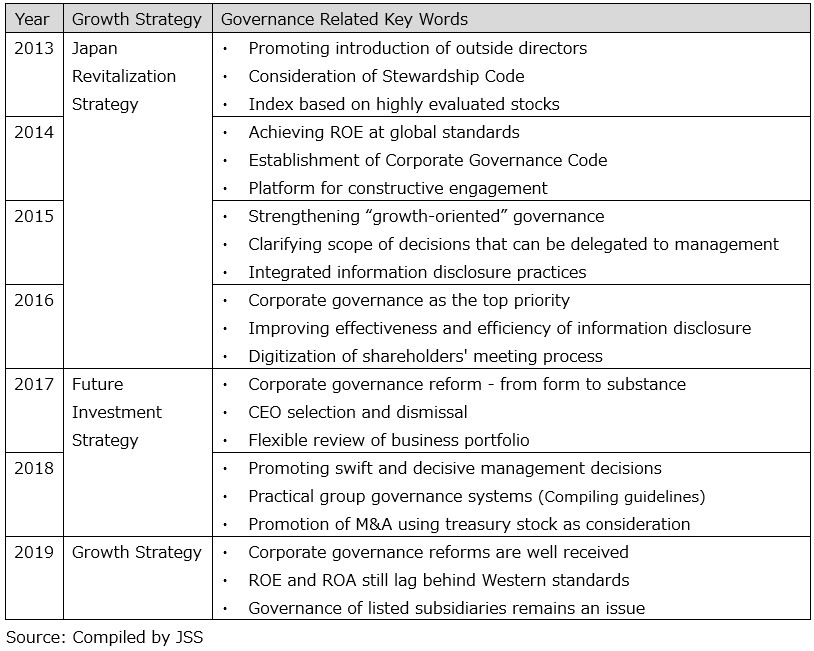

The economic policy of the second Abe administration, known as Abenomics, aimed to reposition Japanese companies as competitive players in the global economy by introducing corporate governance that prioritizes shareholder value, a fundamental principle of global capital markets. It could be said that this was the first economic policy in Japanese history aimed at ensuring the proper functioning of the capital market. Abenomics outlined “three arrows” to achieve escape from deflation and expansion of wealth. In the “Japan Revitalization Strategy – JAPAN is BACK”, which outlined the growth strategy as the third arrow, reforms and transformations of corporate governance were proposed as measures to strengthen the international competitiveness of Japanese companies.

The specific measures proposed in the 2013 recommendations were “promoting the introduction of outside directors” and “strengthening the role of institutional investors.” Both measures aimed to incorporate the perspective of shareholders into companies. External directors were expected to act as proxies for shareholders to oversee management, while institutional investors were urged to directly engage with corporate management. In response, the following year's “Japan Revitalization Strategy Revision 2014 – Challenges for the Future” set “achieving global-level ROE” as a benchmark and outlined various measures to be implemented. A representative action was the introduction of the Corporate Governance Code by the Financial Services Agency and the Tokyo Stock Exchange. Since its formulation in 2015, it has been revised twice, in 2018 and 2021, and listed companies have been encouraged to actively implement it. In addition, various other legal reforms and government-led initiatives have been carried out.

Figure 4-1-2: Corporate Governance in the Abenomics Growth Strategy

Such “government-led governance” has garnered significant support from foreign investors, contributing greatly to the improvement of Japanese companies' evaluations and the increase in their market capitalization. The Asian Corporate Governance Association (ACGA), an international organization of institutional investors, ranked Japan's corporate governance second among 12 Asian countries in its 2023 survey (with Australia in first place), praising it as “a real grab-your-popcorn moment” (Note 5). This likely reflected a high evaluation of the foundation set in place in Japan's stock market for companies and shareholders to share the fruits of enhanced shareholder value together. However, the report also cautioned that the “romantic ending we hope for” – the outcome investors anticipate – is still yet to come, likely due to concerns over persistently low P/B levels.

4. Activists as evangelists of market discipline

Activist investors are the most radical embodiment of the capital market's demand for shareholder value and corporate governance. In early 2000s Japan, where cross-shareholdings provided protection and the logic of institutional investors had not yet fully taken root, activist investors were unfairly labeled as “vulture investors” and viewed as enemies of society. However, in recent years, with the backing of government-led governance initiatives, they have significantly enhanced their influence and ability to act within the capital markets. From the perspective of prioritizing shareholder value, the real issue lies with management that fails to enhance capital productivity or develop growth opportunities. In exposing such inadequacies or inaction and demanding fundamental reforms, activist investors should be seen as “evangelists” who restore market discipline, in my view.

Their arguments are becoming more sophisticated. In the past, extreme demands such as immediately distributing idle assets (excess cash, idle land, etc.) as dividends and replacing the entire management team to take control of management were common and were not necessarily agreed by mainstream institutional investors. However, in recent years, there has been a shift toward more logical and reasonable demands, such as strengthening shareholder returns with an eye on appropriate levels of ROE and DOE, and appointing outside directors with expertise in management issues identified through detailed analysis. These demands do not impose excessive burdens on current management or stakeholders and are directly linked to enhancing shareholder value, so they are likely to receive a certain level of support from the capital market as a whole. The voices of activists are not just those of activists.

Even so, activists remain uncompromising in their stance toward companies that continue to undermine shareholder value. A symbolic issue is the “P/B below 1,” with activists harshly criticizing such companies as “unfit to be Prime-Market listed stocks” and “should be delisted from the Standard Market as well.” A P/B of 1 indicates that management lacks the ability to create shareholder value, while a P/B below 1 signifies that the assets owned by shareholders are diminishing. Even for investors other than activists, it is a fundamental principle of corporate governance that shareholders should demand the return of funds and dissolution or sale of the company if it cannot create shareholder value. Companies must once again clearly recognize their raison d'être – their existence is to create shareholder value.

5. The Mission of Corporate Governance in Value Creation

Why has corporate governance, which appears to have established form, failed to deliver substance? I believe that this is because the essence of corporate governance is not understood. To conclude this chapter, I would like to explore the fundamental mission of corporate governance, using a logic that is not typically employed in conventional corporate governance theory.

Imagine a blank canvas: management is an art, creating value by painting a picture called business. However, if that painting is mediocre or trite, it would not yield value commensurate with the materials and effort invested. In such cases, it might be more beautiful and valuable to leave the canvas blank and untouched. Corporate governance is precisely about serving as a quality patron: demanding management's resolve to “paint a picture” from a “zero-based” perspective, confirming the process from conception to methodology and design, thereby creating valuable art to share with the world.

When management lacks the visual skills or conceptual ability to produce persuasive sketches, corporate governance must determine that such art should not be created. Furthermore, even if the concept is superb, considering the risk that the execution may not proceed as planned, it may be preferable to leave the canvas blank, as this allows one to enjoy its inherent beauty. Schopenhauer famously stated that “All life is suffering,” advocating antinatalism. Similarly, if shareholders view “all management as risk,” they might conclude that funds should be returned to them before any damage occurs and that the company should not exist in the first place.

On the one hand, while being overly risk-averse, shareholder value is not created, and the global economy continues to shrink and stagnate. This could lead to the realization of what Schopenhauer referred to as the “Negation of the Will to Life,” resulting in something akin to “the City of God Against the Pagans” – a state that might resemble human extinction. However, risk is not merely destructive; it is essential for creating value. No matter how brilliant the strategy or how skilled the execution is, there is no such thing as a business manager who can achieve 100% success in value creation. Perhaps the kind of management that leads one to say, “Well then, once more!” as Nietzsche, the affirmation of birth, might have said, is what is needed. I believe that the ability to coldly yet affirmatively assess the intrinsic value of a company is what is now required as the “essence” of corporate governance in modern Japanese companies.

(Note 1) Ministry of Economy, Trade and Industry. Corporate Value Study Group. Corporate Value Report. 27 May 2005,

https://www.meti.go.jp/policy/economy/keiei_innovation/keizaihousei/pdf/houkokusyo_hontai_eng.pdf.

(Note 2) Ministry of Economy, Trade and Industry. Ito Review of Competitiveness and Incentives for Sustainable Growth – Building Favorable Relationships between Companies and Investors – Final Report. Aug. 2014,

https://www.meti.go.jp/policy/economy/keiei_innovation/kigyoukaikei/ito_review__released_august2014_en.pdf.

(Note 3) Ministry of Economy, Trade and Industry. Guidelines for Corporate Takeovers. 31 Aug. 2023,

https://www.meti.go.jp/press/2023/08/20230831003/20230831003-b.pdf.

(Note 4) Ministry of Economy, Trade and Industry. Discussion Results of the “Round Table Conference on Improving of Sustainable Corporate Value” Compiled as “Chair’s Interim Report.” 26 Jun. 2024,

https://www.meti.go.jp/english/press/2024/0626_001.html.

(Note 5)Asian Corporate Governance Association. CG Watch 2023 Overview – Biggest ranking reshuffle in 20 years. 13 Dec. 2023,

https://www.clsa.com/wp-content/uploads/2024/03/CG-Watch-2023-Overview-A-new-order_-Biggest-ranking-reshuffle-in-20-years-20231213.pdf.